Building a smoother AA flow on India’s gold standard

Account Aggregators (AAs) are India’s big bet on open banking—licensed NBFCs that let customers securely share financial data from banks and other regulated institutions with FIUs for use cases like loans, wealth management, and personal finance.

Sahamati is the industry alliance that brings together AAs, FIUs, and FIPs to define how AA should feel for customers: transparent, empowering, and easy to use. In collaboration with partners like IDEO Last Mile Money, they’ve published reference journeys and design principles that many teams now treat as the gold standard for AA consent flows in India.

My goal: take a bloated, dated AA integration and bring it closer to that gold standard—fewer steps, clearer consent, and a flow that feels proudly Indian, RBI-compliant, and AA-native.

When a “simple” flow stopped feeling simple

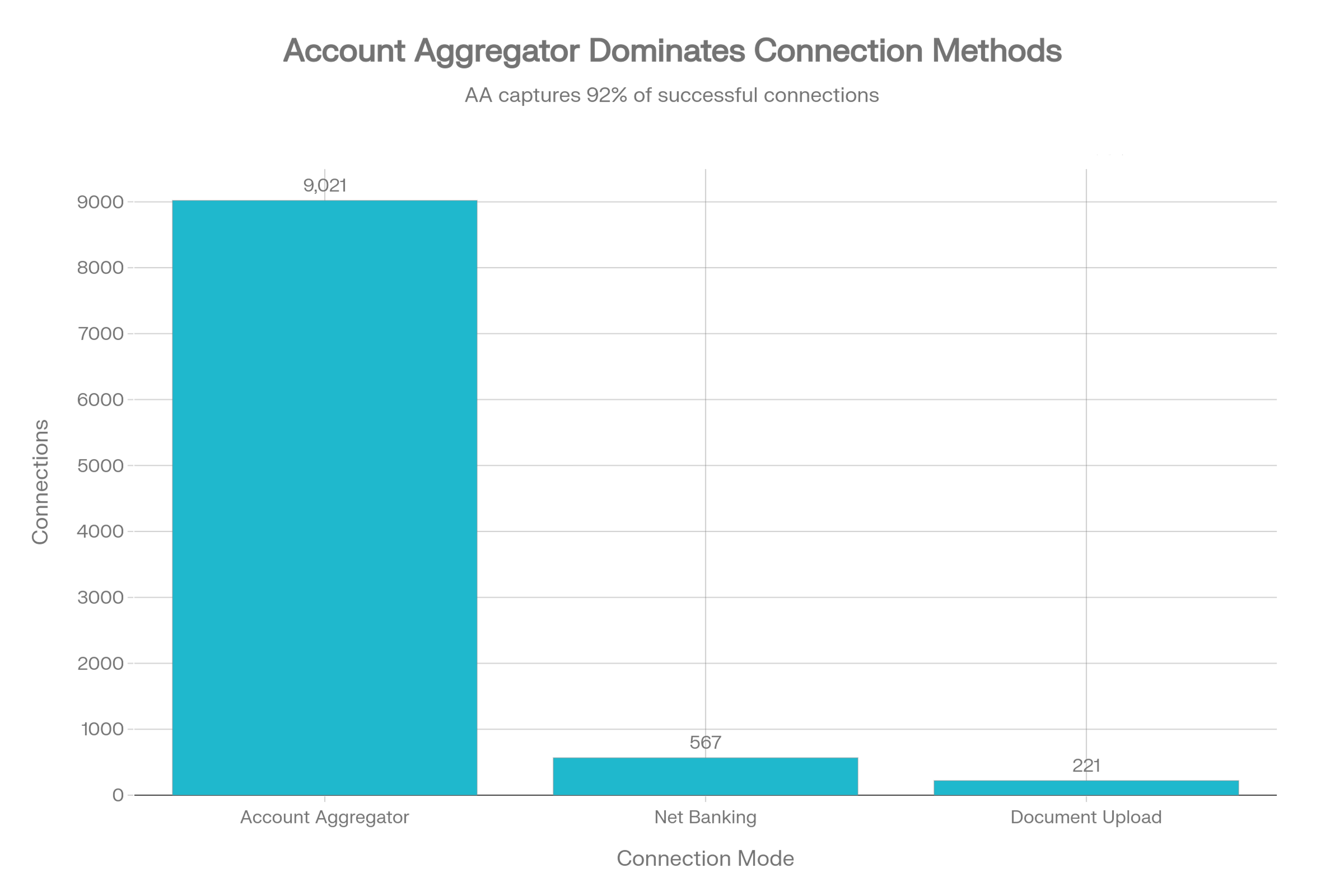

In our product, users connect their salary accounts mostly through Account Aggregator using their phone number and OTP. Alternate modes like Net Banking or statement upload existed, but over 90% of users chose AA.

On paper, the flow was straightforward. In reality, it looked like this:

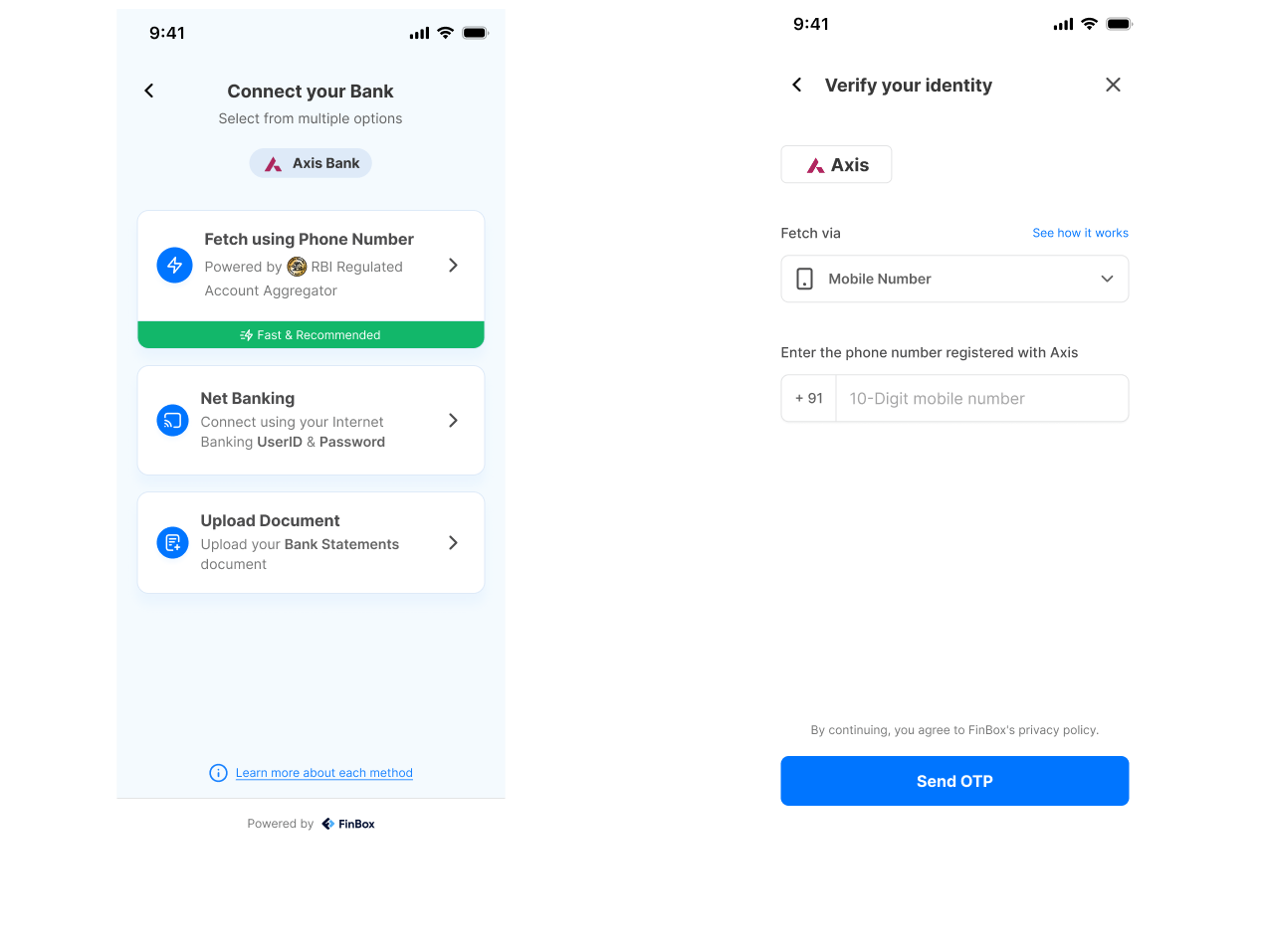

- Bank selection

- Mode selection (Account Aggregator / Net Banking / Upload)

- Phone number input

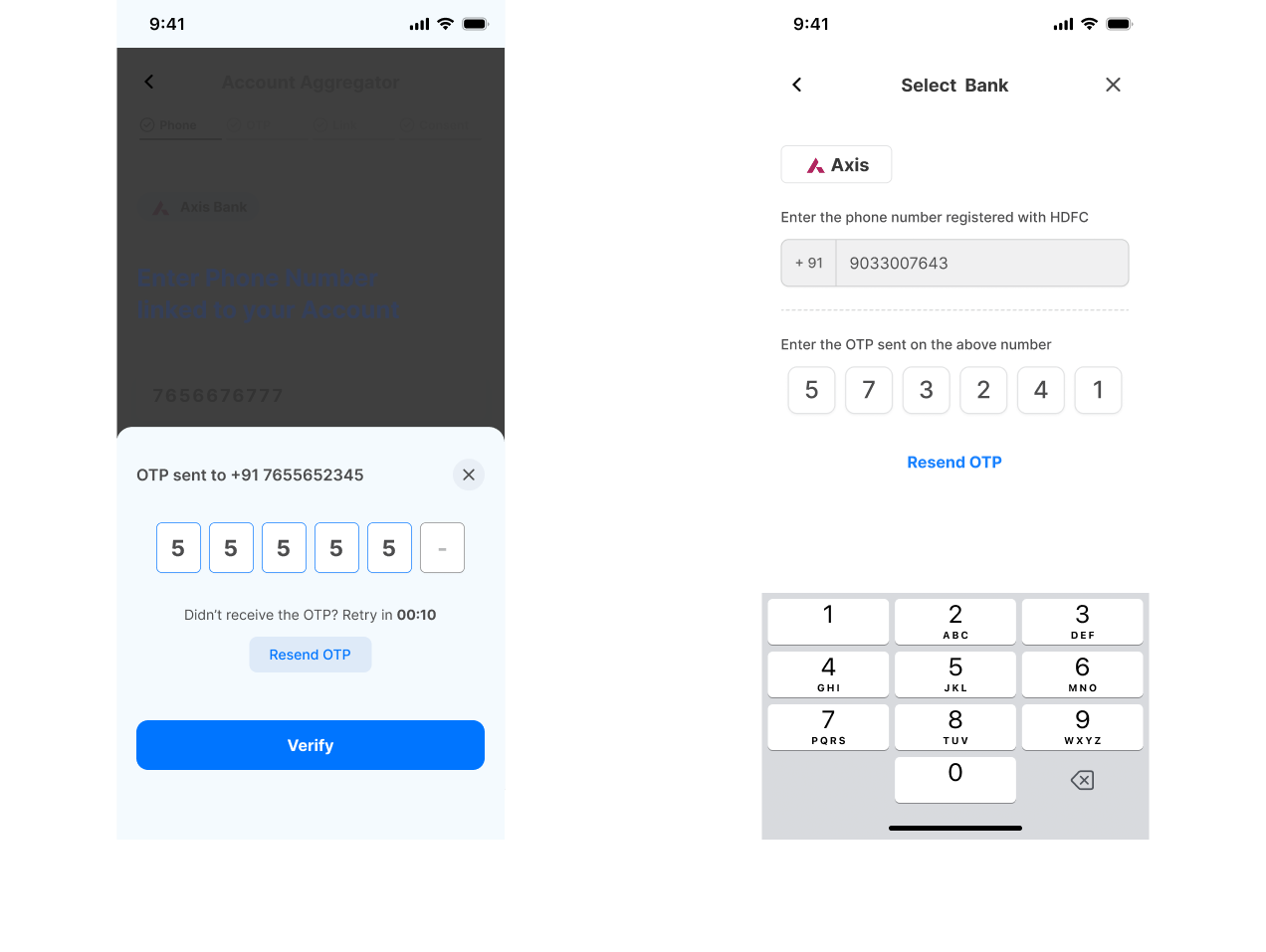

- OTP in a separate bottom sheet

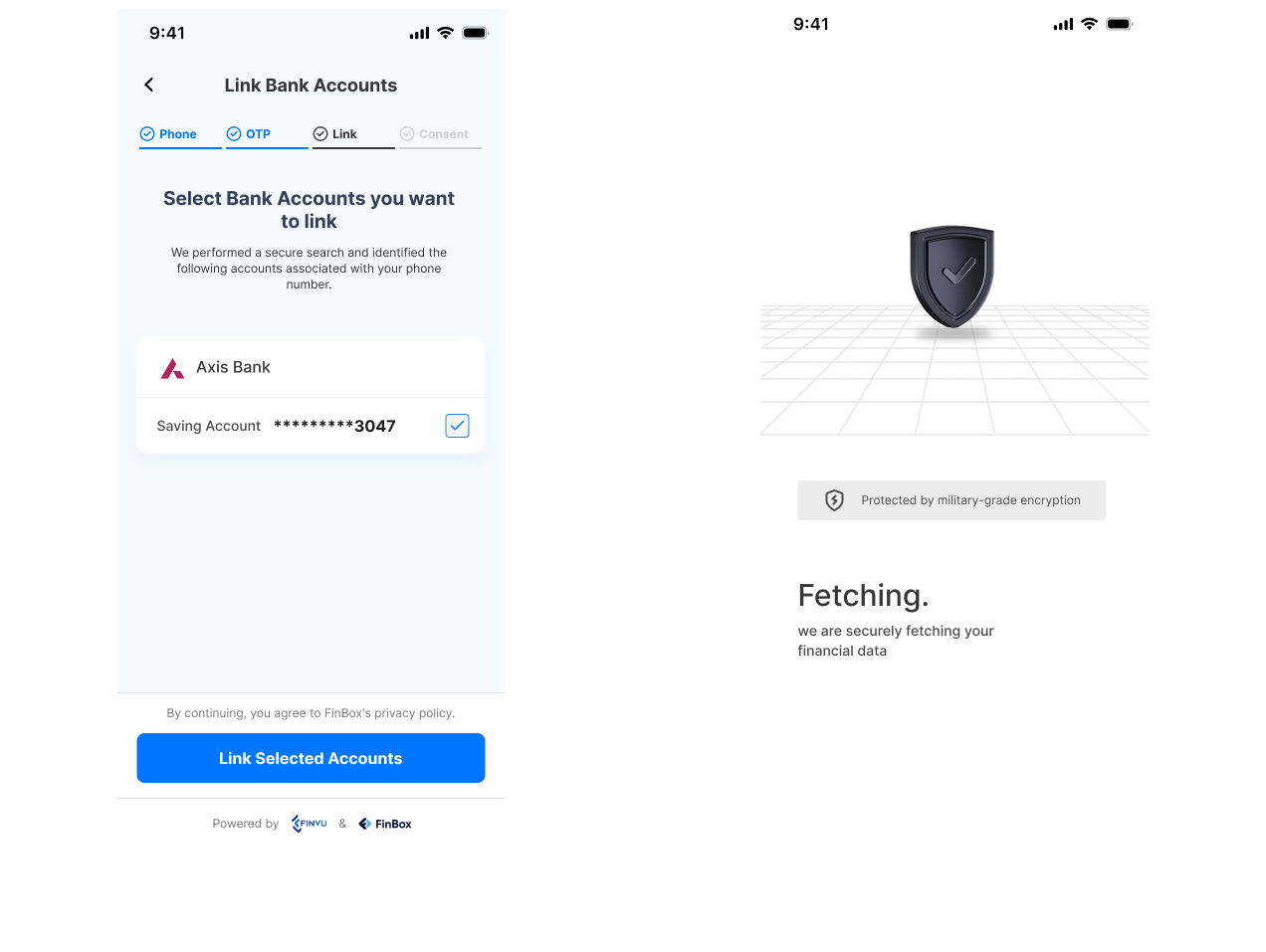

- Account selection (even with a single account)

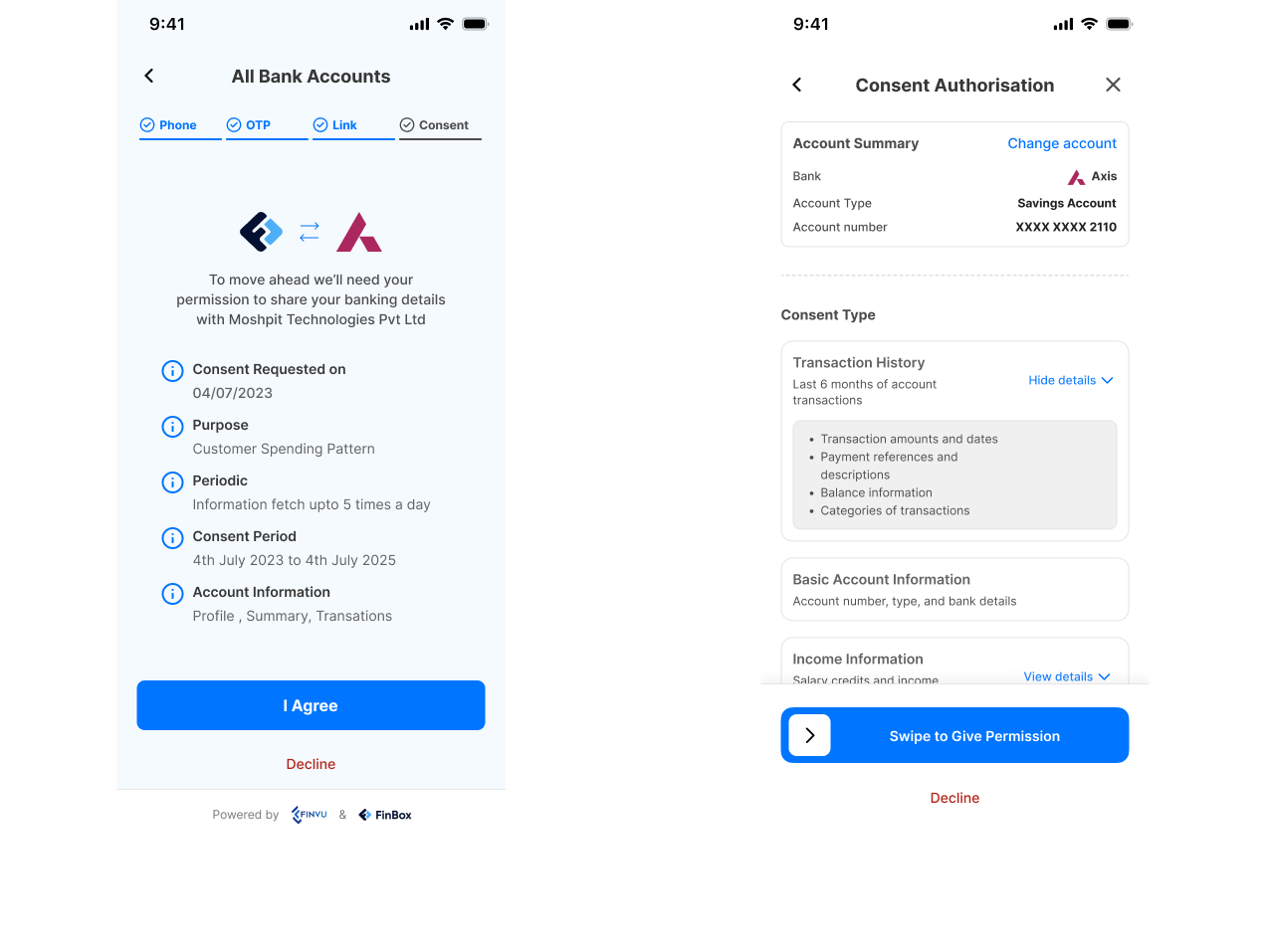

- Dense consent screen

- Basic success state

Visually, the UI leaned on odd fonts, hard shadows, and heavy layouts that didn’t match the trust stakes of handling Indian financial data.

Design challenge

Make connecting a bank via AA feel fast and trustworthy, while staying aligned with Sahamati’s design report and RBI’s expectations on explicit, informed consent—without adding complexity.

Grounding the redesign in Sahamati’s AA standard

Before changing flows, I anchored myself in three things from the Sahamati + IDEO report:

- What AAs are and why they matterAAs are licensed NBFCs under RBI, launched in 2021, enabling safe, digital financial-data sharing for millions of accounts in India.

- Sahamati’s roleSahamati is the industry collective that convenes AAs, FIUs, and FIPs and publishes reference AA journeys, consent checklists, and design principles for the ecosystem.

Core design principles of an “ideal” AA flow

- →Educational, with progressive awareness of consent

- →Trustworthy, signaling safety and RBI authorization

- →Empowering, with meaningful control (including revocation)

- →Transparent, without cognitive overload

What I set out to achieve

I framed the work around three outcomes:

Untangling the original journey

I mapped the existing flow from “Connect bank” to “Account linked successfully,” then overlaid Sahamati’s reference AA journey to see where we diverged.

Original path in our product

Reference AA journey (Sahamati)

Two big gaps emerged:

- We were inflating steps that didn’t matter (mode selection, redundant account selection).

- We weren’t fully leaning into AA’s educational, transparent consent story that Sahamati emphasizes.

Insight 1: Default to Account Aggregator, India’s rails for open banking

Data and product context were clear: Account Aggregator wasn’t just an option—it was the experience for the vast majority. Yet we still made users stop and choose between “Account Aggregator,” “Net Banking,” and “Upload Document.”

AA captures 92% of successful connections

Design move: Hide the choice, keep the control

Dedicated screen asking “How do you want to connect?”

Account Aggregator becomes the default mode, surfaced as a dropdown choice on the main “Connect your bank” screen.

Net Banking and document upload remain available for regional or edge cases but are visually secondary.

Result: One whole screen removed for most users, and one less decision to overthink.

Insight 2: OTP shouldn’t feel like a separate mini‑app

Sahamati emphasizes reducing cognitive load and making flows feel like coherent journeys. Our OTP experience split identity verification into two contexts: one screen for phone entry, one bottom sheet for OTP.

Design move: Keep verification in a single, responsible context

- Phone number input and OTP now live on the same screen.

- After “Send OTP,” the OTP field appears inline.

- Bank identity and RBI/AA partners acknowledged in calm, secondary positions.

Insight 3: Don’t ask for choices when India’s AA rails already made one

In practice, many users have only one eligible account. Still, we forced them to tap the only visible account.

Design move: Conditional account selection

When we discover just one account → skip the selection screen entirely, auto-progress.

When there are multiple accounts → show the selection UI.

Insight 4: Consent in an Indian AA flow must be readable, revocable, and real

Sahamati and RBI are clear: AA is about explicit, informed consent and user agency. Our old consent screen was technically compliant but visually dense.

Design move: Turn consent into an Indian‑context decision point

- Lead with purposeClear statement of what user is sharing and why.

- Expose parameters in chunksSummary at top, data categories in collapsible accordions.

- Make consent deliberateReplaced “I agree” with a “Swipe to Give Permission” interaction.

- Highlight controlClear messaging that users can revoke consent.

The new journey: an Indian AA experience that feels like one clear decision

Compared to the reference AA flow from Sahamati, integration now echoes several key moments:

- Introduce AA in context, not as jargon.

- Keep eligibility and mode logic lightweight but clear.

- Handle account discovery and selection with minimal cognitive load.

- Make final consent readable, revocable, and deliberate.